Business Finance: Moving past rejection

Table of Contents

Making sure that your business has everything it needs to grow and maintain day-to-day operations is a vital responsibility that can either make or break your venture. That’s why it can be very frustrating if you’ve been rejected for business finance. But rather than letting yourself feel intimidated by the situation and draw upon your own savings instead, you should know that rejection needn’t be the end of the road. In fact, it could be the beginning of a whole new one. Thanks to the growing prominence of the Alternative Finance industry, you now have access to more business finance solutions than ever before, regardless of your size or sector. So to improve your chances next time and receive the funds your business needs to go forward, here are 3 steps you need to take.

1. Request an explanation for why your application was rejected

Although it’s gut-wrenching to receive a rejection, it’s important that you fully understand what factors lead to that outcome. As such, you should request an explanation as to why your business was turned down. Sometimes it could be that the product was inappropriate, there was an issue with adverse credit, a lack of sufficient collateral, missing documents or even the way in which your business operates. Whatever the reason may be, you need to be informed so that you’re prepared next time around.

2. Check your credit profile

Before applying for business finance, one thing you need to do is generate a credit report for your business, which can be carried out using one of the UK’s leading credit agencies: Equifax, Experian or Trans Union (formerly Callcredit). This is an important step as it will allow you to review your current financial situation and identify any issues that may be affecting your score. Just some of the details your report should outline may include:

- Your accounts (e.g. credits cards and current accounts)

- Current and past addresses

- How much of your credit limit you regularly use

- Existing finance arrangements

- Late payments

- Accelerated Payment Notices (APNs)

- Past Insolvencies

- Past and recent CCJs (County Court Judgments)

- And whether you have a history of resolving debt on time

However, it’s also worth noting that not every business finance product takes your credit profile into account when making a decision, but possessing an adverse credit rating will affect how much interest you’re charged, reflecting the amount risk the lender is taking on should they accept your application. As such, reviewing your report and taking steps to improve your credit rating beforehand could save you money in the long run.

3. Decide whether or not to provide collateral

This depends on the type of finance you’re thinking about applying and whether it’s Secured or Unsecured. If you possess unencumbered assets (equipment, machinery, vehicles or property), you could use these to present as collateral as part of a Secured finance agreement. Doing so may increase lender confidence which, in turn, could allow you to borrow more capital and gain a favourable interest rate. However, presenting collateral also means putting assets at risk of repossession should your business default.

On the other hand, Unsecured finance agreements do not involve the use of collateral but this exposes the lender to more risk, which may make it harder for you to qualify (especially with an adverse credit rating). It’ll also lead to your business being charged more interest (compared to a Secured agreement). Therefore, you need to think carefully about whether you possess suitable assets and how comfortable you are putting them at risk.

4. Review what Alternative Business Finance solutions are available

Finally, having gone over the details that may have affected your previous application and fine-tuning your approach, you can begin reviewing what types of business finance products are available to you. Although your previous application may have been made using the traditional route, exploring what alternative products and lenders are available could prove more fruitful. As such, by applying for Alternative Business Finance, you could gain access to anything from Secured and Unsecured Business Loans, Overdraft Replacement, Commercial Mortgages, Bridging Loans and Invoice Finance to Merchant Cash Advance. Therefore, being reject needn’t be an obstacle standing your way. In fact, it could be an opportunity in the waiting.

Looking to apply for Business Finance?

Being rejected for finance can be frustrating for any business. It can leave you feeling alone and confused, uncertain of which way to turn next. However, its vital that you don’t let this setback deter you from pursuing your goals. If you’ve got a vision that you’re passionate about achieving, taking a different approach and exploring what the Alternative Finance industry has to offer could be the solution. All you need to do is source an appropriate agreement from a lender you can trust.

At Rangewell, we’re an Access to Finance specialist who’s mapped over 400 lenders to offer you an overview of more than 23,000 business finance products. Our services are free to use and we’ll also guide you through the application process. So if you’re looking to raise for your business, apply for Business Finance today or find out more with Rangewell.

You may be interested in...

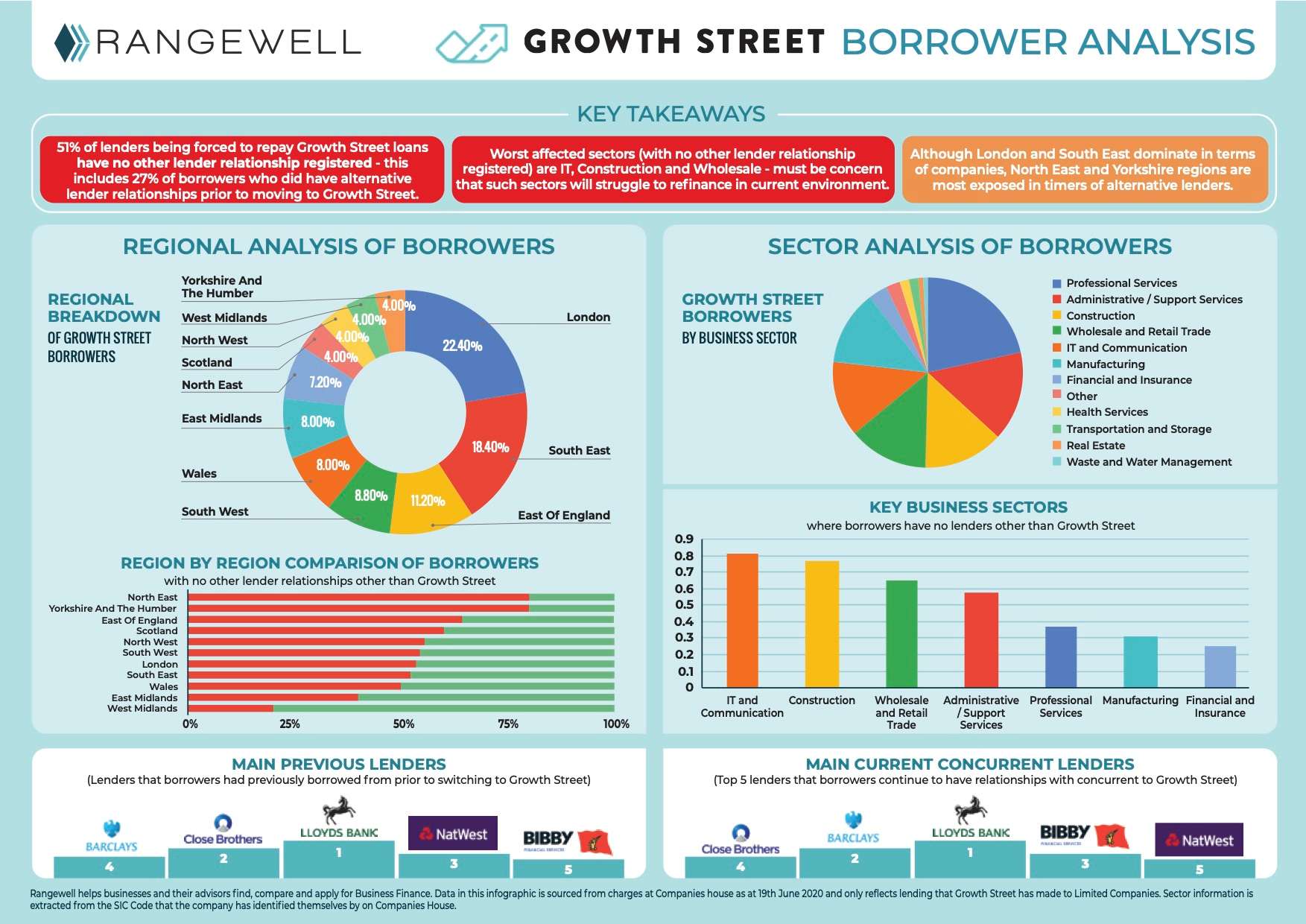

Growth Street Borrower Action Group Launched to support Borrowers

Click here to view the full analysis of Growth Street Borrowers carried out by Rangewell Since Growth Street anno...

22 June 2020

Support My Business

Rangewell has launched ‘Support my Business’, a pro-bono project which aims to help SMEs weather some o...

16 March 2020

What does Capital mean in business?

In order to take your business from A to B there’s a vital resource that you simply can’t do without - capit...

31 December 2018

External Sources of Finance: What are the Advantages and Disadvantages

At every stage in your business’ development, you’re going to need the support and reassurance that can only be found by...

30 October 2018