Top tips for applying for Peer-to-Peer Lending

Table of Contents

As an SME owner, growth is certain to be at the top of your agenda. However, without the funds to back you up, achieving your short and long-term goals can feel like a remote possibility. Yet if you’ve been turned down for finance from the more traditional routes, there are other pathways available that could help. One such funding opportunity that might pique your interest is Peer-to-Peer (P2P) Lending. Peer-to-Peer Lending enables you to appeal directly to a panel of third-party investors across an online platform and convince them of the viability of your business, products and services. However, although outside of your local high street bank, Peer-to-Peer platforms will still exercise the same level of due diligence, with investors expecting to make a return on their investment all the same. So if you’re considering Peer-to-Peer Lending, here are a few tips you need to consider.

-

Make sure that your accounts are in order

Before applying to a Peer-to-Peer platform, you must ensure that your business’ accounts are in order and any relevant paperwork has been correctly filed on time. Note that some platform may even require you to provide an accounting history extending for as far as 2 or 3 years. So if you’re applying for a Peer-to-Peer Loan, getting your business’ accounts straight and preparing any necessary documents beforehand is essential.

-

Clearly present your business’ finances

Another aspect to consider is your business’ finances. Before submitting an application, analyze your business’ income and outgoing expenses. If your outgoing expenses are more than your monthly income this would indicate negative working capital and, if things don’t change, financial difficulty in the near future. In addition, investors will want to see evidence that you’re managing to settle your financial obligations (Utility bills, Tax, Credit Card debts, etc) on time. Plus, investors will also want reassurance that your accounts are being effectively managed, with a clear representation of your business’ Turnover and Profit Forecasts. As such, employing the use of digital account management software such as Xero, Zoho Books and Wave Accounting can be highly beneficial.

-

Check your Credit Profile

If you do choose to apply for Peer-to-Peer Lending, note that the platform and any interested investors will want to have permission to review the Credit Profiles for both your business and any associated directors. They can do this by approaching credit agencies such as Experian, Equifax and TransUnion, which will enable them to gain a stronger understanding of where your business as a whole stands financially. So when carrying out their checks they will incorporate into their search whether you have any CCJs, Accelerated Payments, Arrears, Unpaid Debt and a history of settling debt on time. Should they discover any issues, this may well affect the strength of your credit score and result in either a rejection or more interest being applied to any funds that you acquire. So checking your Credit Report and making improvements wherever possible beforehand could increase your chances of getting accepted by the platform.

-

Explain why your business needs the money

As well as showing that you’ve got a strong grasp on your business’ finances and accounting practices, investors will also want to know more about why your business needs the funds in the first place. Are you looking to expand your current facilities, create new products, bring in new equipment or support your working capital? Whatever the reason may be, investors will want to know how their funds will be used for, the viability of your goals and, above all, the likelihood of them making a return on their investment.

Although Peer-to-Peer Lending is generally a type of short-term business finance, both the platform and any interested investors will want to how you’re going to repay the loan. Such agreements are typically settled using fixed monthly repayments over an agreed term that can last up to 12 months, plus interest.

-

Decide which assets to provide as security

Depending on the platform, you may need to provide Security. If so, you can do this by presenting unencumbered assets such as equipment, machinery, vehicles or property as collateral. Note that if your business defaults, these assets can be repossessed and sold at auction in order to recover the money that’s owed to your investors. Meanwhile, Unsecured Peer-to-Peer Loans require no such commitment but may carry a larger interest rate. However, for additional protection, you and your associated directors may need to provide either a written or verbal Personal Guarantee before the loan can be given.

Thinking about applying for Peer-to-Peer Lending?

At the early stages of your company’s development, you may feel like the number of business finance solutions available to you is limited. However, there are plenty of funding opportunities around that could help, you just need to discover them. One such funding opportunity that’s great for developing SMEs is Peer-to-Peer Lending. This form of business finance allows you to appeal directly to investors and convince them to provide funds for your business. Because of how Peer-to-Peer Lending operates in this regard, there’s no set limit to how much money your business could borrow. However, in order to reap the full benefits of this form of lending, you need to source an appropriate platform for your business. If you’re looking to raise fund in order to support growth, innovation and sustainability, apply for Peer-to-Peer lending today or find out more with Rangewell.

You may be interested in...

Growth Street Borrower Action Group Launched to support Borrowers

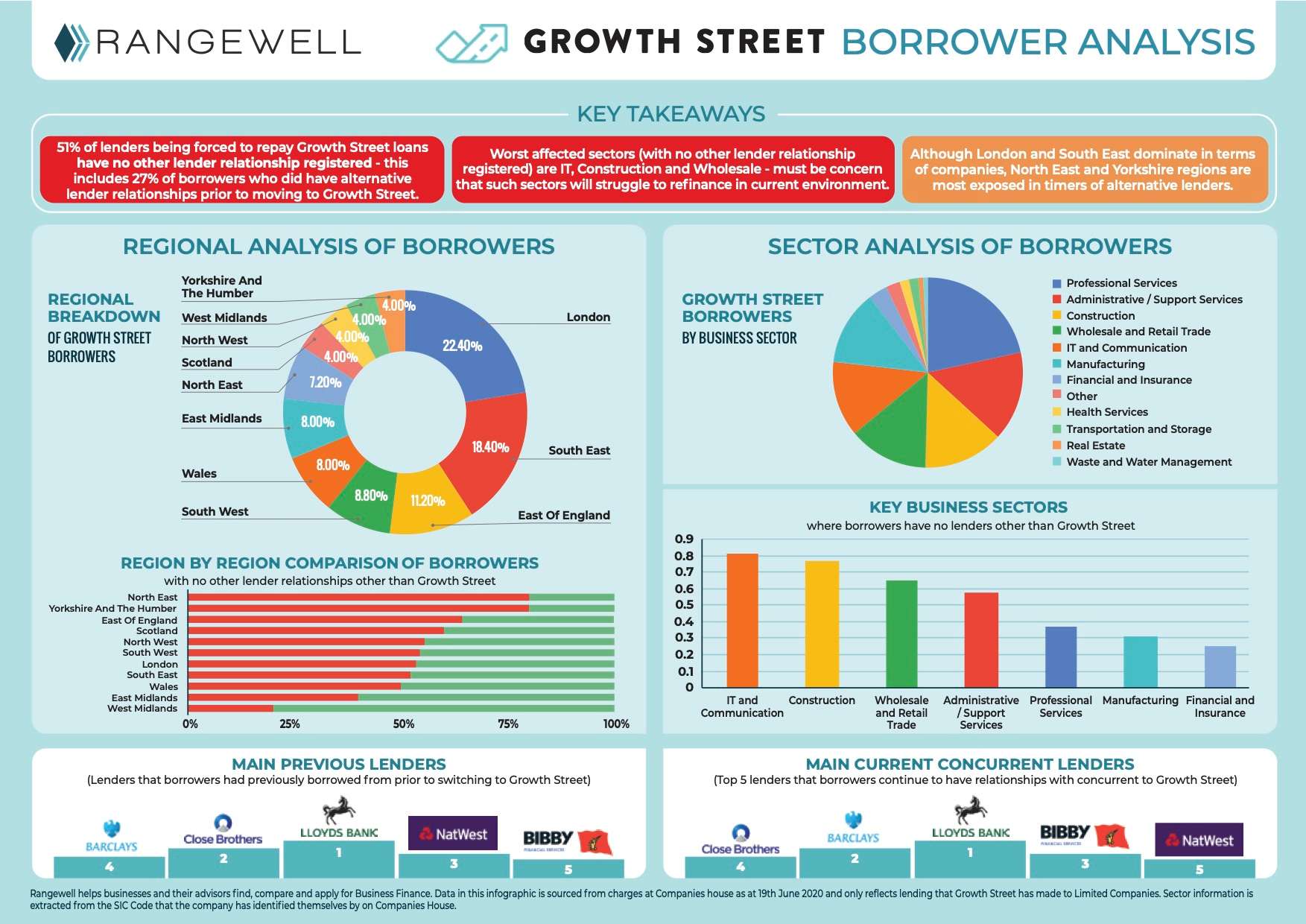

Click here to view the full analysis of Growth Street Borrowers carried out by Rangewell Since Growth Street anno...

22 June 2020

Commercial Mortgages: Advantages and Disadvantages

Buying a commercial is a huge investment, and one that can often only be made with a commercial mortgage. Before you sig...

5 September 2019

CBILS Success Story: £4m lifeline for a student accommodation business

Arranging a £4 million lifeline for a student accommodation business TL:DR All kinds of business have been hit ha...

23 October 2020

What does Capital mean in business?

In order to take your business from A to B there’s a vital resource that you simply can’t do without - capit...

31 December 2018