How to negotiate better rates for Alternative Finance

Table of Contents

If you’re looking to grow, innovate or support your business, seeking out external funding opportunities can often be crucial. However, despite the necessity, many UK SMEs are still unaware of how they can invest in the future of their business. This is both unfortunate and entirely avoidable, thanks to the growing presence of the Alternative Finance industry. Offering access to a diverse range of business finance solutions, the Alternative Finance industry is simply another pathway towards ensuring the success and sustainability of your business. But if you’ve been rejected whilst seeking more traditional forms of funding, the experience may have left you feeling anxious, especially when it comes to the overall cost of finance. Yet with the right support and guidance, negotiating an affordable business finance agreement isn’t as difficult as it may first seem.

Have you checked your Credit Rating?

Before applying for Alternative Finance, check both your personal and business' credit profile with one of the leading credit agencies, eg. Experian, Equifax, and Callcredit, since lenders will use this information to decide how much interest they will charge. By thoroughly assessing the report that they generate, you’ll gain a stronger understanding of how you appear financially. Does it show if you have outstanding or past CCJs, Accelerated Payment Notices, arrears, unpaid debts or a reliable history settling debt on time? Should you notice any incorrect details, contact the concerned credit agency as soon as possible whilst providing sufficient proof to show that your financial situation has changed. Even a misspelt address can negatively affect your credit rating.

Do you have any savings?

If you have any noteworthy savings, you can use this to negotiate more favourable interest rates. Lenders are always looking for ways to minimise the amount of risk they’re accepting should your business default. So by showing lenders how much you have saved, you can argue that you’ll be able to keep up the concerned repayment scheme, even if you have a temporary decline in cash flow.

Can you fund a portion of the project or goal yourself?

If you have any personal savings, you can use this to your advantage in yet another way. Although some products, such as Commercial Mortgages, require you to place equity as standard, using a portion of your own funds to support a project could make your application more attractive. This is because it will demonstrate to lenders that you have a strong interest in ensuring that the agreement is fully repaid on time, whilst reducing the number of funds that you’ll need to borrow.

However, you should avoid funding business projects entirely with your own funds as doing so can cause any number of issues which can affect your future growth and sustainability.

Are you able to provide collateral?

When considering business finance, you need to decide whether you want to use a Secured or Unsecured finance solution. Using a Secured product means offering up unencumbered assets (equipment, machinery, vehicles or property) as security, which is generally looked upon more favourably by lenders. Although this can help if you gain a lower interest rate and borrow larger lump sums, this also means putting assets at risk of repossession should your business default on the agreement. Meanwhile, finance solutions that are Unsecured do not require you to offer security, which can be useful if you don’t currently own any assets or prefer not to put them at risk. However, such agreements usually arrive with larger interest rates and can harder to acquire, especially with adverse credit.

Could you offer lenders a Personal Guarantee?

Another way you can improve lender confidence, borrow larger lump sums or gain a lower interest rate is by offering lenders a Personal Guarantee. A Personal Guarantee is either a written or verbal declaration of your intention to fully repay the agreement on time. But you also need to be fully aware of what this entails. If your business defaults on the agreement, the lender may choose to pursue you and any associated directors for the remaining sums.

Are there any additional costs and fees you need to be aware of?

In addition, make sure that you’re clear on where there are any additional costs and fees involved. Just some of these costs could involve set-up, administration and legal fees to Missed Payment Penalties, Redemption Penalties, Exit Fees and Balloon Payments. In order to be clear on the overall cost the agreement, thoroughly check all of the documents provided by the lender. If you have any further questions, you can also arrange to have a face-to-face meeting with the lender as well. Plus, you should also compare what other lenders may be charging for a similar product. Doing so can put you in a stronger position during negotiations and, perhaps, allow you to reduce or even negate some of these costs entirely.

Thinking about applying for Alternative Finance?

Searching for business finance can be daunting. With so many products to choose from, sourcing business finance on your own isn’t easy. Although you might choose to go down the traditional route, doing so may not yield the results that you desire. However, before you decide to draw funds from your own accounts, why not consider how the Alternative Finance industry could help? Granting you access to a wide range of business finance products and lenders, exploring this constantly developing industry could be what you need to ensure the success of your business. All you need to choose a product suitable for you.

At Rangewell, we have Access to Finance specialist working with over 350 lenders to offer you an overview of more than 23,000 business finance products. Our services are free to use and we’ll also guide you through the application process. We’re with you every step of the way. So if you’re looking to grow your business and need help acquiring the necessary funds, apply for Alternative Finance today or find out more with Rangewell.

You may be interested in...

Growth Street Borrower Action Group Launched to support Borrowers

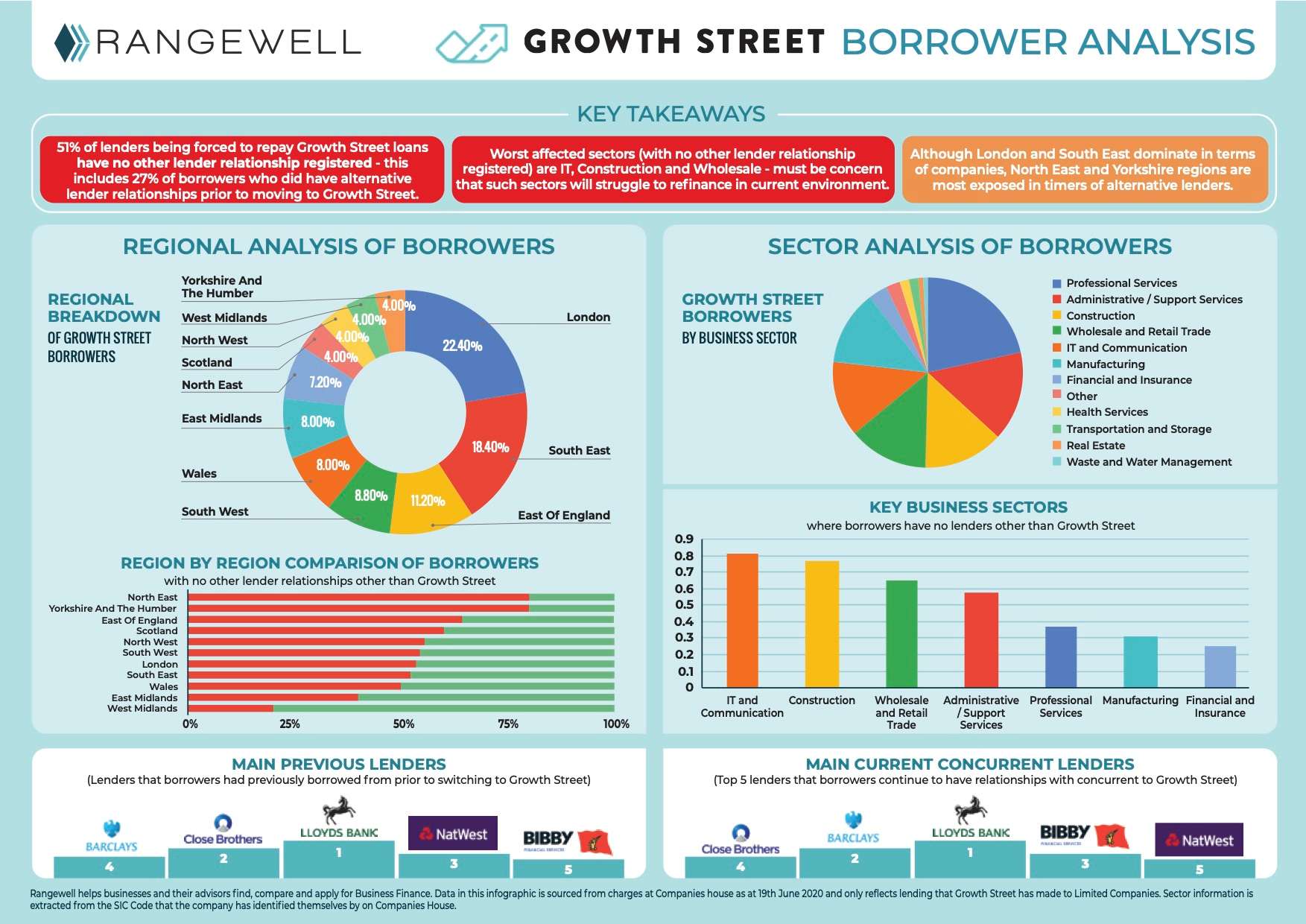

Click here to view the full analysis of Growth Street Borrowers carried out by Rangewell Since Growth Street anno...

22 June 2020

Commercial Mortgages: Advantages and Disadvantages

Buying a commercial is a huge investment, and one that can often only be made with a commercial mortgage. Before you sig...

5 September 2019

Growth Guarantee Scheme lending surges as challengers outpace the big banks

Our latest analysis reveals that lending under the Government’s Growth Guarantee Scheme (GGS) has surged by 79% in...

15 September 2025

Securing £250,000 Funding for A New Dental Practice

Expanding is always costly, but when it makes good business sense, you need reliable funding solutions for every challen...

19 September 2019